Navigating the Ohio USDA Loan Landscape: A Comprehensive Guide

Related Articles: Navigating the Ohio USDA Loan Landscape: A Comprehensive Guide

Introduction

In this auspicious occasion, we are delighted to delve into the intriguing topic related to Navigating the Ohio USDA Loan Landscape: A Comprehensive Guide. Let’s weave interesting information and offer fresh perspectives to the readers.

Table of Content

Navigating the Ohio USDA Loan Landscape: A Comprehensive Guide

The United States Department of Agriculture (USDA) offers a variety of loan programs designed to support rural development and promote homeownership. These programs, often referred to as "USDA loans," are particularly beneficial for individuals and families seeking to purchase or improve properties in eligible rural areas. Understanding the intricacies of these programs, especially in the context of Ohio, requires navigating a complex landscape of eligibility criteria, loan types, and geographical boundaries. This guide provides a comprehensive overview of the Ohio USDA loan map, its significance, and the resources available to potential borrowers.

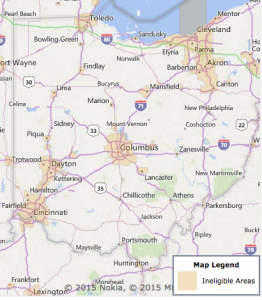

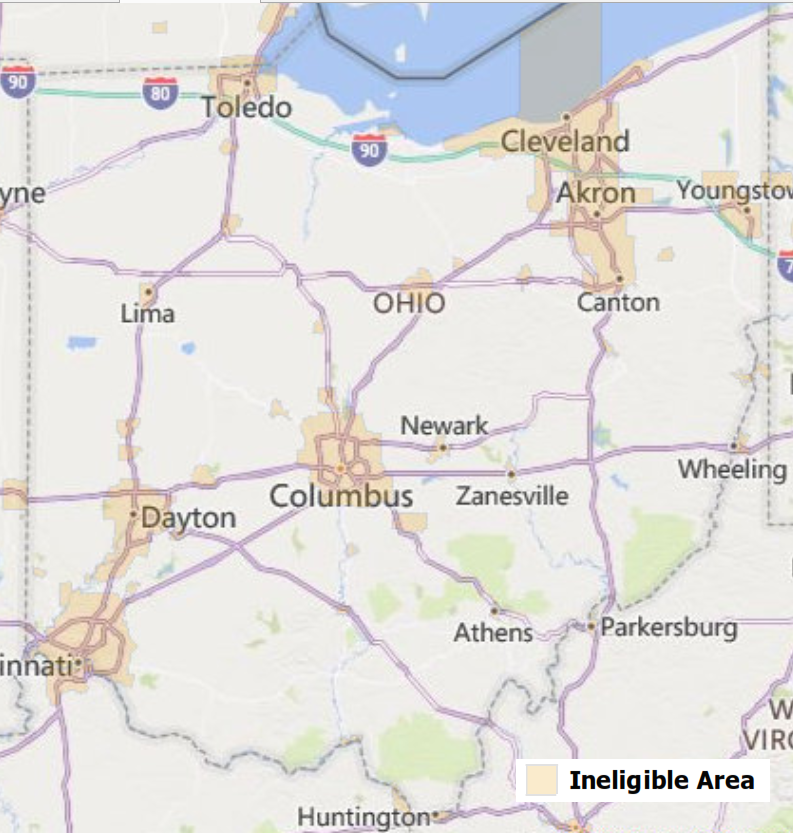

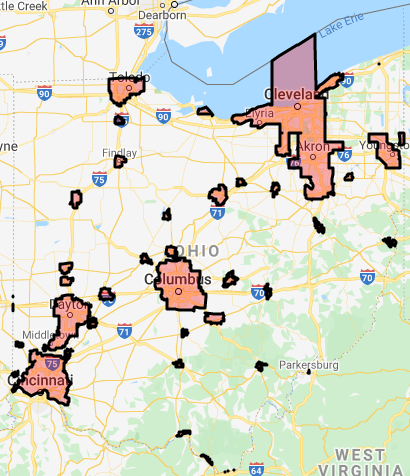

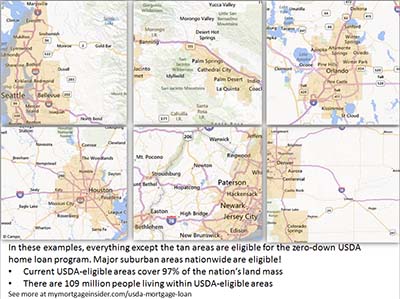

Decoding the Ohio USDA Loan Map:

The USDA Rural Development program defines "rural" based on specific population density and other factors. This definition translates into a visual representation known as the "USDA Loan Map." This map delineates eligible areas within Ohio, highlighting those where USDA loan programs are available.

The map is a crucial tool for prospective borrowers, offering a clear visual representation of where their property falls within the USDA’s eligibility criteria. This information is critical for determining whether a borrower qualifies for USDA loan assistance, which can significantly impact the feasibility of their homeownership aspirations.

Understanding the Benefits of USDA Loans in Ohio:

USDA loan programs offer several distinct advantages for eligible Ohio residents, making them a valuable resource for aspiring homeowners:

- Lower Interest Rates: USDA loans typically have lower interest rates compared to conventional mortgages. This translates into lower monthly payments, making homeownership more accessible for individuals and families with limited financial resources.

- Lower Down Payment Requirements: USDA loans often require a significantly lower down payment compared to conventional mortgages. This can be a game-changer for borrowers who struggle to accumulate a substantial down payment, allowing them to enter the housing market sooner.

- No Private Mortgage Insurance (PMI): Unlike conventional mortgages, USDA loans do not require PMI, which is an added insurance policy protecting lenders against potential losses. This eliminates a significant financial burden for borrowers, further reducing overall loan costs.

- Flexible Credit Requirements: USDA loans may be more lenient with credit requirements than conventional mortgages. This offers a lifeline for borrowers with less than perfect credit histories, allowing them to access homeownership opportunities that might otherwise be inaccessible.

- Support for Rural Communities: USDA loans play a vital role in fostering economic development and promoting community growth in rural areas. By facilitating homeownership and revitalizing rural communities, these programs contribute to a more balanced and prosperous state.

Navigating the Different USDA Loan Programs:

The USDA offers a diverse range of loan programs, each with its own set of eligibility criteria and specific requirements. Some of the most common programs available in Ohio include:

- Single-Family Housing Direct Loan Program: This program provides direct loans to individuals and families for the purchase or improvement of single-family homes in eligible rural areas.

- Single-Family Housing Guaranteed Loan Program: This program offers loan guarantees to lenders, enabling them to provide loans to eligible borrowers with more favorable terms.

- Rural Housing Repair Loan Program: This program provides loans to low- and moderate-income homeowners for essential repairs and improvements to their existing homes.

- Rural Development Loan Program: This program offers loans to businesses, organizations, and communities in rural areas to support economic development and job creation.

Accessing the Ohio USDA Loan Map:

The Ohio USDA Loan Map is readily available online through the USDA Rural Development website. This interactive tool allows users to search for specific areas within Ohio, identify eligible zip codes, and view detailed information about USDA loan programs available in those areas.

FAQs about the Ohio USDA Loan Map:

Q: What are the eligibility requirements for USDA loans in Ohio?

A: To qualify for a USDA loan in Ohio, borrowers must meet specific income and credit requirements. They must also reside in an eligible rural area as defined by the USDA. Additionally, the property being purchased must be located in an eligible area and meet specific USDA standards.

Q: How can I find out if my property is eligible for a USDA loan?

A: You can utilize the online USDA Loan Map to search for your property’s zip code and determine its eligibility. Alternatively, you can contact a local USDA Rural Development office or a USDA-approved lender for assistance.

Q: What are the income limits for USDA loans in Ohio?

A: Income limits vary based on the size of the household and the location within Ohio. The USDA website provides a detailed income chart outlining these limits.

Q: What are the interest rates and loan terms for USDA loans in Ohio?

A: Interest rates and loan terms for USDA loans in Ohio are subject to change based on market conditions. However, USDA loans generally offer lower interest rates than conventional mortgages and have longer repayment terms, typically up to 30 years.

Q: How do I apply for a USDA loan in Ohio?

A: To apply for a USDA loan, you must work with a USDA-approved lender. These lenders are familiar with the program’s requirements and can guide you through the application process.

Tips for Successful USDA Loan Applications:

- Research thoroughly: Understand the eligibility requirements, loan programs, and application process before applying.

- Seek professional guidance: Consult with a USDA-approved lender to ensure you meet all eligibility criteria and navigate the complex application process effectively.

- Maintain good credit: A strong credit history is essential for securing a USDA loan.

- Prepare your documentation: Gather all necessary documentation, including income verification, credit reports, and property information.

- Be patient: The USDA loan application process can take time, so be prepared for delays and potential hurdles.

Conclusion:

The Ohio USDA Loan Map serves as a vital tool for individuals and families seeking to access homeownership opportunities in rural areas. By understanding the program’s eligibility criteria, benefits, and application process, potential borrowers can make informed decisions and leverage the resources available to achieve their housing goals. The USDA’s commitment to rural development and affordable housing makes these programs a valuable asset for individuals and communities throughout Ohio, fostering economic growth and strengthening the fabric of rural life.

Closure

Thus, we hope this article has provided valuable insights into Navigating the Ohio USDA Loan Landscape: A Comprehensive Guide. We thank you for taking the time to read this article. See you in our next article!