Navigating the Landscape of Rural Texas: A Guide to USDA Loan Eligibility

Related Articles: Navigating the Landscape of Rural Texas: A Guide to USDA Loan Eligibility

Introduction

In this auspicious occasion, we are delighted to delve into the intriguing topic related to Navigating the Landscape of Rural Texas: A Guide to USDA Loan Eligibility. Let’s weave interesting information and offer fresh perspectives to the readers.

Table of Content

Navigating the Landscape of Rural Texas: A Guide to USDA Loan Eligibility

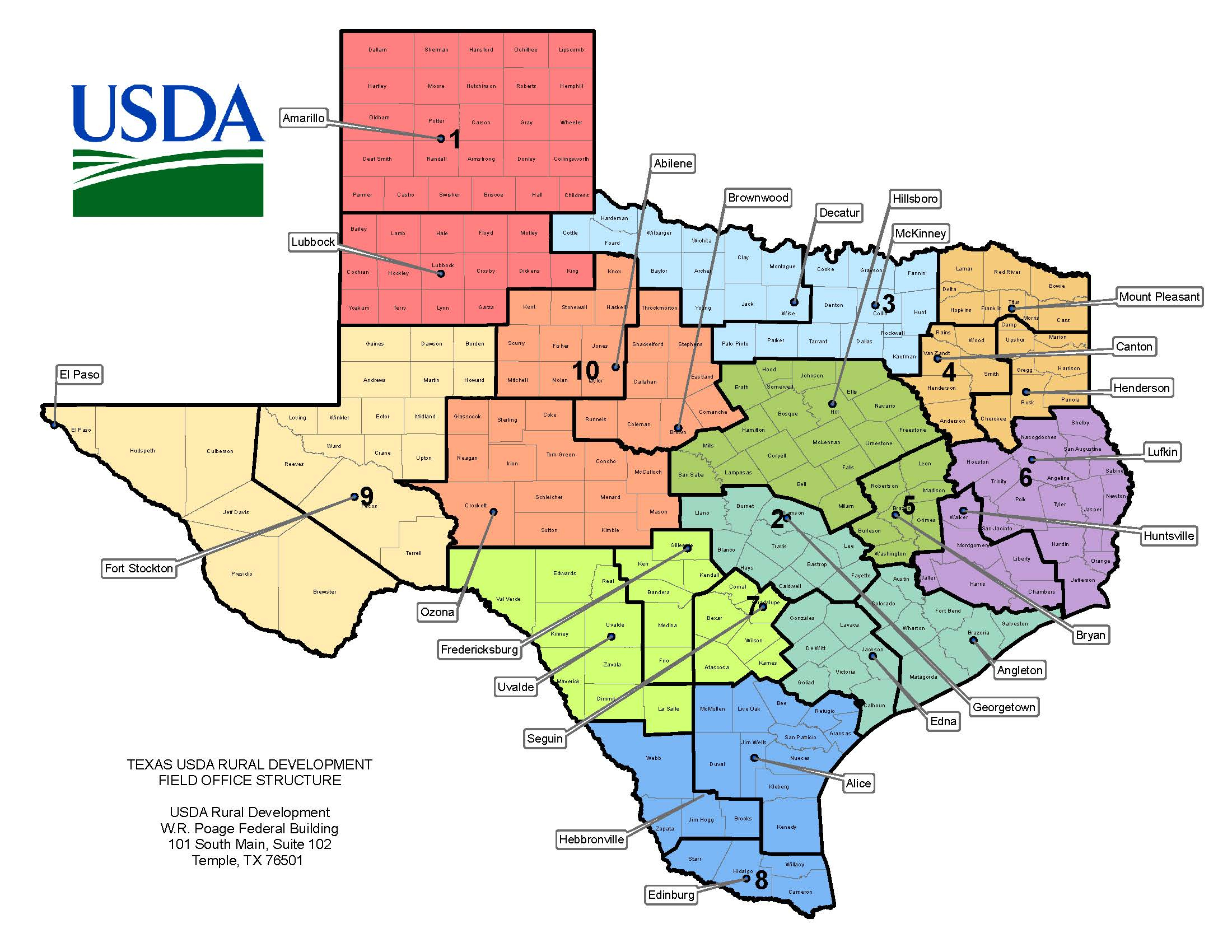

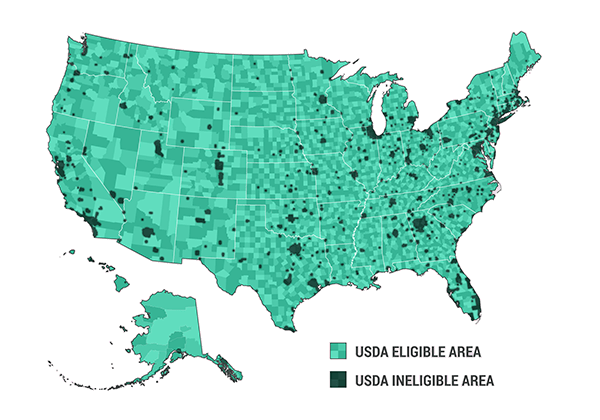

The United States Department of Agriculture (USDA) offers a range of loan programs designed to support rural development and promote homeownership in eligible areas. These programs, collectively known as USDA Rural Development Loans, are particularly beneficial for individuals seeking to purchase or refinance homes in rural communities. Understanding the geographic scope of these programs is crucial for potential borrowers, as eligibility is determined by location. The USDA Loan Texas map serves as a visual guide to identify areas where these programs are available.

Decoding the USDA Loan Texas Map

The USDA Loan Texas map is an interactive tool that visually delineates eligible areas within the state. It utilizes a color-coded system to distinguish between eligible and ineligible zones. Typically, eligible areas are shaded in green, while ineligible areas are marked in gray. The map can be accessed on the USDA Rural Development website or through various third-party platforms.

Understanding Eligibility Criteria

While the map provides a quick visual overview, it is essential to remember that eligibility is determined by a combination of factors, not solely location. The USDA defines "rural" as areas outside of metropolitan cities and towns with populations exceeding 20,000. However, specific criteria vary depending on the loan program.

Key Factors Influencing Eligibility:

- Population Density: The USDA considers population density, with areas generally considered rural if they have a population density of less than one person per acre.

- Distance from Metropolitan Areas: Areas located outside of a certain radius from major cities are typically considered eligible.

- Property Type: Eligibility is often contingent on the type of property, with programs typically focusing on single-family homes, multi-family units, and farm properties.

- Income Limits: USDA loan programs often have income limits based on household size and location. These limits vary across different regions and programs.

- Property Value: There are often maximum property value limits for USDA loans, which vary based on the loan program and location.

Benefits of USDA Loans in Texas

USDA loans offer several advantages for eligible borrowers in Texas:

- Lower Down Payment Requirements: USDA loans typically require a down payment of only 0% for eligible borrowers, making homeownership more accessible.

- Competitive Interest Rates: USDA loans often have interest rates comparable to conventional mortgages, offering cost-effective financing options.

- Flexible Credit Requirements: The USDA program considers credit scores and debt-to-income ratios more leniently than some conventional lenders, providing opportunities for borrowers with less-than-perfect credit histories.

- Rural Development Support: By providing access to affordable homeownership, USDA loans contribute to the economic growth and revitalization of rural communities in Texas.

Navigating the Application Process

Applying for a USDA loan involves several steps:

- Pre-Approval: Before beginning the application process, it is recommended to obtain pre-approval from a USDA-approved lender. This helps determine eligibility and provides an estimated loan amount.

- Property Search: Use the USDA Loan Texas map to identify eligible properties within your desired area.

- Loan Application: Submit a complete loan application to a USDA-approved lender, including documentation such as income verification, credit history, and property details.

- Loan Approval and Closing: Once the application is approved, the lender will schedule a closing process, where you will sign the loan documents and finalize the purchase of the property.

Frequently Asked Questions (FAQs) about USDA Loans in Texas

Q: What is the maximum property value for a USDA loan in Texas?

A: The maximum property value for a USDA loan varies based on location and program. It is recommended to contact a USDA-approved lender for the most up-to-date information on property value limits in your specific area.

Q: Can I use a USDA loan to refinance an existing mortgage?

A: Yes, USDA loans can be used for refinancing purposes. The program offers a variety of refinancing options, including Streamline Refinance and Rural Housing Repair Loans.

Q: What are the income limits for USDA loans in Texas?

A: Income limits for USDA loans vary based on household size and location. You can access the USDA Rural Development website or consult with a USDA-approved lender to determine the specific income limits for your area.

Q: How do I find a USDA-approved lender in Texas?

A: The USDA Rural Development website maintains a list of approved lenders in each state. You can also consult with local real estate agents or mortgage brokers for recommendations.

Tips for Securing a USDA Loan in Texas

- Start early: Begin the pre-approval process early to determine your eligibility and obtain a pre-approval letter.

- Shop around: Compare loan terms and interest rates from multiple USDA-approved lenders to find the best options.

- Understand your credit score: A higher credit score generally leads to more favorable loan terms.

- Prepare documentation: Gather all necessary documentation, including income verification, credit reports, and property details, to expedite the application process.

- Seek professional guidance: Consult with a real estate agent and a USDA-approved lender for personalized advice and support throughout the process.

Conclusion

The USDA Loan Texas map provides a valuable resource for individuals seeking to purchase or refinance homes in eligible areas. By understanding the program’s eligibility criteria, benefits, and application process, potential borrowers can navigate the path to homeownership in rural Texas. Accessing these programs can contribute to the economic growth and revitalization of rural communities while offering affordable and accessible homeownership opportunities.

Closure

Thus, we hope this article has provided valuable insights into Navigating the Landscape of Rural Texas: A Guide to USDA Loan Eligibility. We thank you for taking the time to read this article. See you in our next article!